Global sharemarkets were skittish in May as a

result of concerns that the US Federal Reserve (“US Fed”) may begin plans to

remove the quantitative easing measures in place designed to stimulate the US

economy.

With medium term targets for unemployment of 6.5%

and inflation of 2%, the US Fed is clearly seeking to stimulate growth in

the economy; through the continuation of a near zero funding rate

(0%-0.25%) and

Federal Open Market Committee purchases of about

$45 billion per month in Treasury securities and $40 billion per month in

mortgage backed securities. These measures appear to be having the desired

effect, with March quarter GDP ticking up to an annualised growth rate of 2.4%,

whilst inflation remains well under target at 1.1%. Unemployment remains high,

but has fallen to 7.6% (at the end of March).

Consumer confidence has also risen to its highest

level since 2007, and in the corporate sector, balance sheets have been progressively

repaired as a result of the cheap financing rates. This ongoing improvement in

the US economy and stronger balance sheets has also translated in an

improvement in listed company earnings per share (“eps”). In fact, the eps of

listed businesses in the US now exceed 2007 levels.

Trailing EPS Since 2007 Peak

Source: Citi Research, Trailing EPS Since 2007

Peak, May 2013

In the psyche of markets however, the corollary of

an improving US economy is the question of likely changes to quantitative

easing and monetary policy. Bond markets have already started to react, with 10

year US government bond yields rising 46 basis points in May.

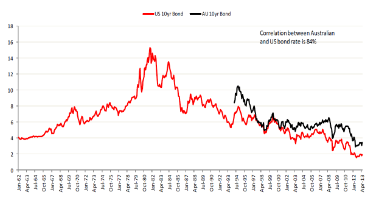

Interestingly, Australian 10 year bond yields rose

26 basis points over the same period, highlighting the high level of

correlation between the markets (further illustrated in the following

chart), and suggesting any

Further changes in US Fed stimulus and yields will

directly influence bond yields in Australia.

Comparing Australian and US rates

Source: Macquarie Research, May 2013

It is clear that once the US Fed becomes

comfortable with the rate and extent of the economic recovery it will begin to

unwind is stimulatory monetary and quantitative easing measures (whilst taking

care not to derail the recovery). As they plan to ‘communicate their

intentions’ we expect bond markets to also unwind - as has already begun.

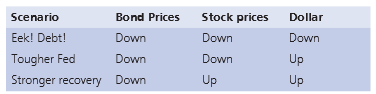

Noted US economist and Professor of Economic and

International Affairs at Princeton University, Paul Krugman, recently offered

an interesting summary of the possible scenarios for US bonds, stocks and the

US Dollar as a result of US Fed, as per the following:

Source: “Rate Stories”, Krugman, May 2013

Indices:

The

Australian All Ordinaries Index has moved up increasing +1.3%

since closing last Friday to 01:10 pm today.

The

rest of the world as measured by the MSCI index increased +3.3%

in A$ from closing last Friday to end of trade Thursday.

Have

a great weekend,

The team at IPS

No comments:

Post a Comment